Parts One and Two established the framework and system to use for the study. Now it is time to get to the meat of the study: How can we combine elements of trend-trading to a system that often trades counter-trend?

First, what measure constitutes the trend? Deciding the best measure for the trend can be somewhat subjective; since many, many traders use the 50 day simple moving average, that is what will be used in this study.

With the 50 day average as our trend indicator, the close must be monitored. If the close is above the 50 day average, we have a long bias. If the close is below the 50 day average, we have a short bias.

The final question then is how to capture the bias? While there are likely many ways, what will be proposed here is a combination of leverage and position-sizing. Thus, if the trade is with the trend (above the 50 day and going long, or below the 50 day and going short), as much as 2x leverage will be used. If the trade is against the trend (long and below the 50 day moving average or short and above the 50 day moving average), the position size will be decreased.

Finally, how will performance be measured to determine if the there are any improvements to the system?

Performance will be measured by 4 criteria: Net Profit, Largest Intraday Drawdown, Largest Trade Drawdown, and Average Drawdown. For each of these calculations, the drawdown figure will be divided into Net Profit to create a ratio.

For example: Net Profit = $10,000 and Largest Intraday Drawdown = $2,000. $10,000 / $2,000 = 5.0

As the ratio increases, the Net Profit is rising and the drawdowns are decreasing. Thus, the higher the ratio the better.

Using the system described in Part Two as the baseline, varying combinations of position-sizing and leverage will be used to trade with the trend while trading against it.

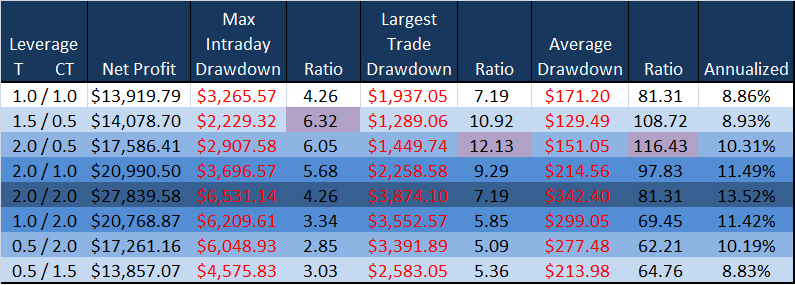

The graph above shows the results. The left most column shows the varying combinations of leverage and trend where T = trend and CT = counter-trend. We see on the first row the results of the baseline system where no leverage or position-sizing were used (T = 1.0 and CT = 1.0).

The second row shows leverage with the trend of 1.5x and a decrease in the position size when trading counter-trend of .5x. Assuming 10K per trade for the baseline system, with the trend a position of 15K is taken, while against the trend only 5K is used.

The third row shows 2x leverage with the trend (20K position) and .5x position against the trend (5K). This row shows the best drawdown ratios (in purple) for Largest Trade Drawdown and Average Drawdown. This version will have a position that is 4x larger with the trend than when trading against the trend.

Already it should be evident that Net Profit is increasing, due mainly to the leverage. However, the ratios show that drawdowns are decreasing. The 2nd row shows a ratio of 6.32 (in purple) which is the highest ratio of the study for max intraday drawdown. By simply using 1.5x leverage with the trend and cutting position-size in half against the trend, Net Profit increases while all drawdown measures decrease. In fact, for the 1.5 / 0.5 row, the largest intraday drawdown and max trade drawdown are decreased by roughly 1/3rd.

The row showing 2.0 / 2.0 is the baseline system using 2x leverage on all trades, regardless of the trend.

After the 2.0 / 2.0 row, the leverage and position-sizing are switched so that now the system is using leverage against the trend and decreasing position size with the trend. Note that Net Profit stays very close while the drawdowns increase (causing a decrease in the ratios).

I believe that the last three rows prove that leveraging with the trend makes up for the lost gains from taking smaller position sizes, while smaller position sizes when trading against the trend improves the drawdown characteristics of the system.

Summary

Beauty is in the eye of the beholder…I like the 2.0 / 1.0 version as net profit is improved by 33% over the baseline system while the drawdown ratios improve 25%, 22%, and 17% respectively.

If one is satisfied with the baseline system and just wants to improve the drawdown characteristics, then the 1.5 / 0.5 version might be appropriate.

Avenues for future research could include using the distance of the close from the trend to calculate more advanced position-sizing / leveraging algorithms. Perhaps the slope of the trend indicator could also guide position-sizing / leveraging.

In Terms of Real Life…

The baseline system gave a long entry signal for Thursday’s (February 19th) open. Had the 1.5 /0.5 version been used, only a HALF position would have been purchased. Based on the recent market action, I would personally feel better about sitting on a half long position rather than a full long position going into Monday.

I may not be understanding the system but the results seem a little distorted because a different amount is risked for each combination. (20K, 20K, 25K, 30K, 40K, 30K, 25K, 20K)

The annualized return seems to match the amount risked so that the 2.0/2.0 (40K total) produces the largest return and the 1.0/1.0 (20K total) combination produces about half as much.

It might be better to use a fixed amount of money that is divided between the trend and counter trend based on the ratios between them. The 2.0/0.5 combination would divide (for example) 40K into 32K/8K positions.

Wood,

Wow, that little bastard really does look like an elf.

If the government talks private equity guys into taking pieces of C and BAC with most likely some behind the doors guarantees that they won’t be raped by goats, I think we see a big pop next week.

As the world continues to burn, no doubt.

Greetings David. The baseline system uses a fixed amount of 10K per trade (with no compounding), and as the testing never assumed more than 2x leverage, then the most risked is 20K. I’m not sure if you’re adding each leg together to get 40K of risk. I wasn’t specific, but the system is either long or short, so there would never be more than 20K risked at any point in time, even with 2x leverage.

Using a fixed amount of money divided between the trend / counter-trend should result in similar drawdown characteristics as what is posted above. The combinations you provided should not result in anything substantially different as that just has you taking larger positions with the trend and smaller positions against the trend.

The difference is that with a fixed 40K, and not using leverage, BOTH returns and drawdowns will be smaller. Unfortunately, taking smaller positions means smaller net profits, unless one is willing to use leverage.

What I was trying to show was a way to decrease the large drawdowns that sometimes happen with mean reversion systems by adding a leveraged trend following component.

This study shows that it is possible to use leverage, achieve greater net profits, while simultaneously improving the drawdown characteristics of the system. Typically, greater net profits mean greater drawdowns, and with the 2.0 / 1.0 version, that is what happens in the study above. However, the ratio shows that the Net Profits increase more greatly than the drawdowns do.

Looking forward to checking you out on Covestor!

Leonard, like a baby, I sold out of my long SPY position Friday, taking a small loss. The bad news, both in the media and what I am seeing happen around me, is starting to get to me.

Odds though continue to favor a bounce.

I still think they will nationalize, but they will call it something else. I was very disappointed to hear the press secretary come out with that statement when the administration knows FULL WELL that nationalization is a possibility. Should they resort to nationalizing after that statement, the public/markets/constituent will trust them even less than they do now.

Told you he looks like an Elf!

Wood, I’m cornfused. If the baseline is 2.0/2.0 which makes profit of $27k and 2.0/1.0 makes $21k profit, how is 2.0/1.0 an improvement of 33% when it’s lower net profit?

Thanks in advance for clarifying.

Aristotle, good question.

The improvement of 33% is over the baseline system 1.0 / 1.0 (the first row in the spreadsheet) where the net profit is 13,919.

The 2.0 / 2.0 is just the baseline system with 2x leverage on each trade.

What we are looking for is an increase in Net Profit with a decrease in drawdowns. The ratio should reflect that relationship. The 2.0 2.0 doubles net profit but your drawdowns double as well.

Anyone could take a system and apply leverage to it, theoretically doubling, tripling, quadrupling returns. The problem is that the drawdowns on a leveraged system can wipe you out if you use too much.

A lot of the problems of leverage are not seen until you begin compounding. This study doesn’t compound as it wants to show purely the effect of varying position sizes in relationship to the trend.

Were this system to use compounding, the largest monthly drawdown would be 17%. If it were to use the 2.0 / 2.0 version with compounding, your drawdown has now doubled to 34%.

Remember, we want the best of both worlds…higher net profits, and lower drawdowns.

Ah, that makes sense. For some reason, I was thinking you were playing both the long and short sides at the same time.

Great article Shed.

This is something I have been wrestling with myself. I know it is more profitable to take trend trades for big points, but those systems are usually 40-50% with larger PF. Compare that to the psychological comfort of 70-90% accuracy, but with a smaller PF. I’m trying to bridge the two bec I think there is a lot to be said for psychological comfort, but it’s no surprise that the more lucrative strategy (losing more, bigger winners) is harder.

OT Question…where’s the BBQ sauce and brass knuckles?

Wood:

This is a real interesting approach to the strength of the bet issue. What you mention about the slope of the trend affecting the strength of the bet (a loss and drawdown) is very important. We’ve all back tested stocks and etfs that are in either primary uptrends or downtrends, and we all know that the trigger “fits” and profit runs are best within the prevailing trend. One thing I’ve tried is to scale the leverage to the number of winning days after the trigger (this is sorta like Danny’s 3 day contrarian rule), and this has been working best within the trend. Counter-trend steps are really nerve racking, because the length of the runs is usually shorter (especially with the rumors and talking heads) in the counter trend. You’re method might accomplish the same thing (or better) with an initial decision rule that you can walk away from. So, I’m definitely going to think about this method.

You might be able to use a 50/200 period single regression channel indicator to pick off the slope data.

The good news is that the CCI indicator for this system will probably trigger a long buy Monday if the Obamarama maniplation works!

Good stuff dude…

Danny, also, counter-trend trading offers more opportunity. So, while one may have been 85%+ accurate shorting every spike since 1/1/08, you still would have made less than if you also bought every dip. However, once you started buying the dips, your accuracy dips to the high 60s% to low 70s%.

As for trend trading being more profitable than mean-reversion, I don’t think that is a fast and hard rule. A good swinging / mean reverting system can actually be more profitable than a pure trend system as a pure trend system doesn’t catch the smaller swings.

Manuel, say more about scaling leverage to number of winning days after the trigger…I’m not sure I understand, but it sounds interesting.

I’ve been toying with regression channels and feel there is promise there but have not put a lot of time into them yet.

True, true. I guess for me it’s different bc my system is…mechanical discretionary? Is that even possible?

Signals trigger my entries, but by system uses a lot of my own discretion (usually for better, occasionally for worse).

Since I am the sole-arbiter, I have to be psychologically comfortable. So do I want comfort, or profit, or ideally both since they are not mutually exclusive. It’s similar to fighting a mechanical system during drawdown. You want to fight it bc drawing down hurts. Most trading mistakes I thin stem from the desire to flee pain right away. Thats why people jump out early, chop around, revenge trade, etc. They want to feel good.

If it was easy and felt good, we’d all be naturals.

Danny, Carstens wrote something about traders who use mechanical signals but also use discretion. I think he called it something like “adding alpha through discretion.” Basically you would initiate the trade based on the mechanical signal, but maybe you double down, or add leverage based on your discretion.

One of the hardest things is to clearly identify your goals and then design the system to meet them. So if your goal is to make as much money as possible as fast as possible, then you are not going to worry about being comfortable, which means you accept your system will have large drawdowns. The opposite of that, as you write, is being comfortable, which means your system will sacrifice large profits in order to have smaller drawdowns. At some point the two do become mutually exclusive, but not until you move more towards the extremems.

But this idea of designing it for your goals is perhaps the most important thing to do as a system that doesn’t work with your goals/personality/psychology is going to fail because it will not be traded as it was designed to be traded.

You are exactly right, and one of the major reasons I started system trading was to quit making so many mistakes that stemmed from fleeing from pain.

“You are exactly right, and one of the major reasons I started system trading was to quit making so many mistakes that stemmed from fleeing from pain.”

same here, just we took different paths and have slightly different (tho quite similar) approaches to suit different temperaments. But yeah, its a realization every trader makes and the sooner the better. “if I knew then what I know now” type of thing

I like that concept of discretionary alpha

Hated how they called out Santeli too… so much for freedom of the press and the new hope… Oh, and good post as per usual. Best, JP

Wood:

Basically, your system is more refined in terms of dollar allocation than what I scraped together at the first of the year. Below is what I’ve been doing with the 403b since then. The disclaimer is that I haven’t done any backtesting, and there haven’t been enough cycles to test drawdown, but I think you have simulalted the data in your table above.

Entry-4/6 SMA cross. Exit has been the downside of W%R(3,8)(your CCI(8) looks like it will do a much better job relative to the W%R). The long 1X is used to generate the long/short signals. It’s always invested; long or short.

I can only use specific funds that are available from the AM, and trading this stuff is extremely frustrating to me, compared to the daily stuff. Longs are RYROX (Russell 1X), RYCMX (Russell 1.5X), RYRLX (Russell 2X). Shorts are RYCBX (S&P 2X), and RYUCX (Russell 1X). I can’t use a corresponding short pair match-up for the Russell because of the AM’s selections.

Right now the ratio of winning short days/long days is about 3:1 with the above signals. One way to look at the trend issue is to think about the ratio of winning short/long days–bigger ratio equals greater downtrend. As a generalization, if the ratio lowers and reverses the trend should go from flat to upward. So, to crudely deal with this I started using the 1X Russell long and the 2X S&P short with equal dollar amounts. If the ratio of winning longs increases in the future, then I’ll start using the 1.5/2x long Russell. So, conceptually I think this is consistent with your system, although probably not maximized. The gains are up about 50% (combined l/s) for the year, as compared to about 38% if the 2x short was bought and held.

For the coming months I definitely want to incorporate your method of dollar allocation in relation to the trend just to see how it works.

On another note, I gotta say that the tabbed posts this weekend are off the scale in terms of “big picture” content. And, if there is an overall theme from Fly, you, Danny, John and others is that you must have a plan and stick to it. You guys are doing a fantastic job of bringing it all home by presenting different approaches to the same end–banking coin…

Well said, finally a good report on this stuff